Global Recycling Day: Analysing the role of scrap in steelmaking through the years

To mark Global Recycling Day, Matthew Wenban-Smith reflects on the history of steel recycling and what it tells us about the transition to a net-zero steel economy in the future.

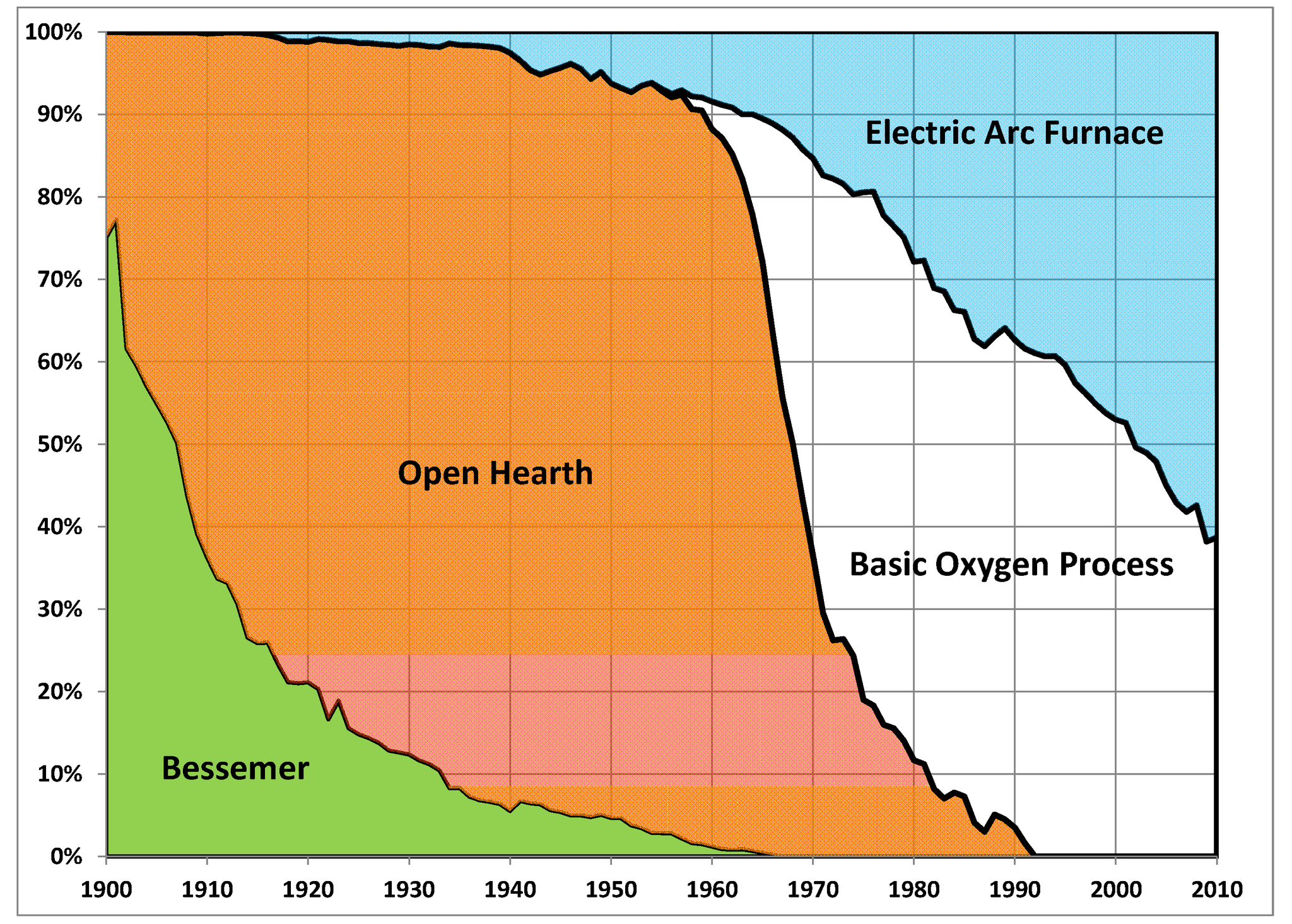

When it comes to recycling, it is worth taking the long view. For the first few thousand years, iron and steel recycling meant reworking rather than re-melting. The development of the blast furnace around one thousand years ago made it possible to convert steel scrap into liquid metal. And the first commercial Electric Arc Furnace (EAF), capable of using 100% scrap, was built in 1906.

Smaller, less costly to build, and more flexible to operate than blast furnaces, the spread of EAFs through the 20th century was limited only by the availability of scrap and electricity.

In the US, as demand for new steel approached saturation and as the steel in infrastructure and buildings constructed 40 or 50 years previously became available for recovery and recycling, scrap-based EAF production began to replace blast furnace steelmaking, even as the blast furnaces themselves used more scrap. Blast furnace production peaked in 1969, and no new blast furnace has been built in the US since 1980 (Construction Physics, 2023). Today, around 70% of steel in the US is made in EAFs (American Iron and Steel Institute, 2021).

The same pattern of increasing demand, met initially from primary production and then later through a growing reliance on scrap, is now playing itself out in Europe and China, is set to take off in south Asia, and it is to be hoped will roll out across Africa. Steel production globally is projected to peak in the second half of the 21st century, with scrap supply following 30 or 40 years after that.

The growth of scrap-based production has been driven by economics, of course, rather than by any concerns about the climate or greenhouse gas emissions – but that doesn’t make it any less welcome. A tonne of steel made entirely from scrap has around one-fifth of the greenhouse gas emissions of a tonne of steel made from iron ore.

Does that mean we can all relax, and recycle our way out of the climate crisis? Sadly not.

The American Iron and Steel Institute (AISI) estimates that the USA now recycles between 70% and 80% of all of its potentially available scrap (AISI, 2021). The World Steel Association (worldsteel) puts the global recycling rate even higher than that, at around 85% for end-of-life scrap.

Then why, despite these impressive recycling rates, is there currently only enough scrap to meet around one-third of the global demand for steel? The main reason is that scrap availability reflects the level of steel production a generation ago, rather than today. Steel production in 1985 was around 720 million tonnes. Today it is around two billion tonnes. Even without taking account of end-of-life recovery and furnace yield losses there is no way to make those numbers add up.

As demand for steel levels off in the future, a higher proportion of that demand will be met from scrap. In its ‘Sustainable Development Scenario’, in which the end-of-life recycling rate rises to 90%, the IEA estimates that there would be enough scrap to meet 45% of the demand for steel in 2050 (IEA, 2020). That is something to celebrate. But to put it the other way around, it would mean that 55% of the world’s steel – perhaps 1.2 billion tonnes of it – would still be made directly from iron ore.

To have any chance of limiting climate change to ‘well below 2 degrees’ and at the same time respecting the aspirations of 9 to 10 billion people, two things therefore need to happen. Firstly, the vast majority of primary steel will need to be made using ‘near zero’ emission sources of iron – using hydrogen-based direct reduction iron (DRI), direct electrolysis, biofuels, carbon capture or other new processes. And secondly, the electricity used in steelmaking will need to be generated with near zero emissions, whether it is used to power electric arc furnaces, hydrogen production, or direct electrolysis.

Those are the twin challenges for policy makers, steelmakers and steel users, and they apply across the whole sector.

To meet those challenges, they, and we, need to be able to compare the GHG emissions performance of all steelmaking on a like-for-like basis, whether steel is made from 100% scrap, 100% primary iron, or from any ratio of inputs in between – an approach pioneered in the ResponsibleSteel Production Standard, and recommended by the IEA, German Steel Association and others.

So let’s hear it for the recyclers, but also for the ‘near zero’ power generators, and the ‘near zero’ iron innovators.

And for a successful transition to a net-zero steel economy.

By Matthew Wenban-Smith

Matthew Wenban-Smith has worked in the area of voluntary sustainability standards and conformity assessment since 1994, when he began working with the newly established Forest Stewardship Council (FSC). In 2006, he founded the independent consultancy OneWorldStandards, providing services to established and emerging sustainability standards initiatives, and completed a variety of projects in the mining, minerals and metals sectors.

Matthew worked for several years with ResponsibleSteel, developing the ResponsibleSteel International Production Standard. He continues to work with ResponsibleSteel and others as a consultant. Read more from Matthew here.